SMM reported on July 10 that during this week (July 4-10, 2025), the total inventory in the two major stainless steel markets of Wuxi and Foshan showed a trend of inventory buildup, increasing from 978,000 mt on July 3, 2025, to 990,800 mt on July 10, up 1.31% WoW.

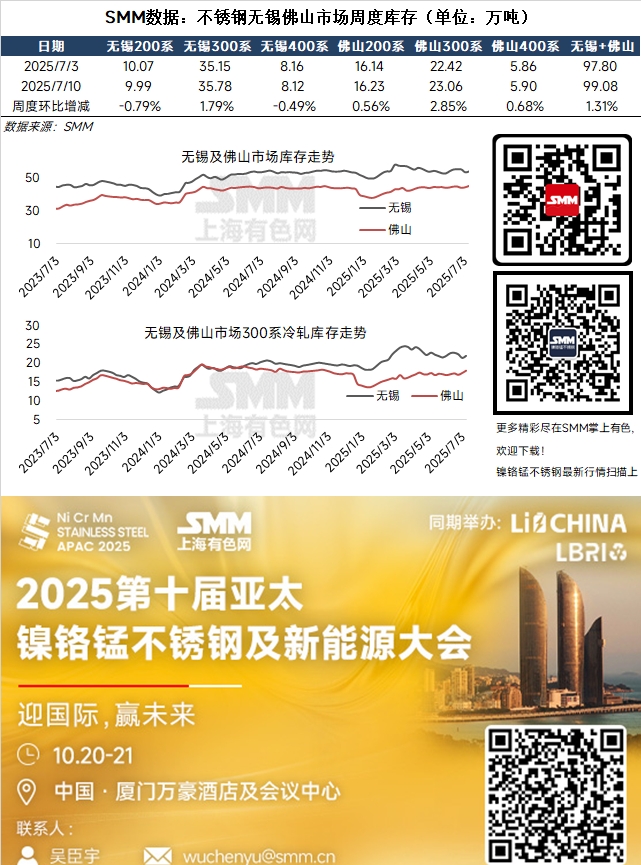

The social inventory of stainless steel ended its previous destocking trend and experienced inventory buildup again this week. Despite the market's temporary surge in transactions stimulated by news of production cuts at stainless steel mills earlier, the in-plant inventory of steel mills accumulated earlier remained high. Additionally, as it is still in the traditional consumption off-season, downstream demand has not truly recovered, and the de-stocking speed of market supplies has been relatively slow. This week, although the futures market rose, the mills' offer prices remained low, and the price ceiling for flat products was also lifted. Steel mills still focused on actively shipping goods, with arrivals remaining high during the week. However, downstream end-users' purchases were still mainly based on immediate needs, and it was difficult to effectively alleviate inventory pressure in the market. Currently, in the traditional consumption off-season, the summer heat has further weakened some downstream demand. Against the backdrop of accumulated inventory at steel mills earlier, it will still take some time for the restoration of supply-demand balance in the stainless steel market and the repair of market confidence.

200-series: Wuxi's 200-series inventory decreased from 100,700 mt to 99,900 mt, a drop of 0.79%; Foshan's 200-series inventory increased from 161,400 mt to 162,300 mt, a rise of 0.56%. 300-series: Wuxi's 300-series inventory increased from 351,500 mt to 357,800 mt, a rise of 1.79%; Foshan's 300-series inventory increased from 224,200 mt to 230,600 mt, a rise of 2.85%. 400-series: Wuxi's 400-series inventory decreased from 81,600 mt to 81,200 mt, a drop of 0.49%; Foshan's 400-series inventory increased from 58,600 mt to 50,000 mt, a rise of 0.68%.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)